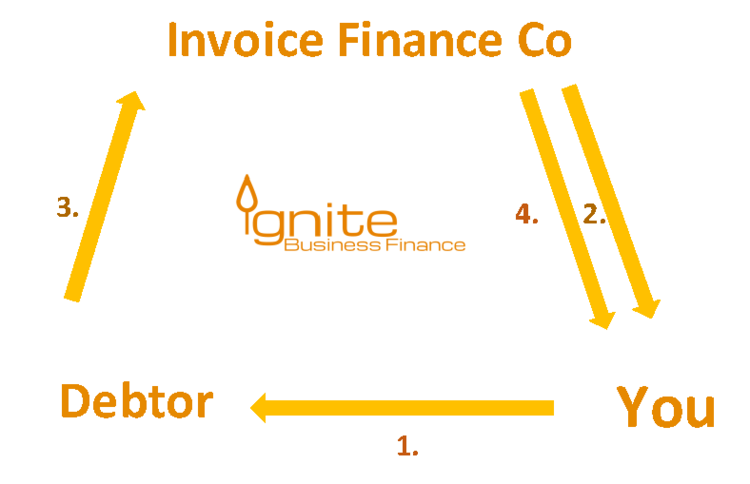

IGF Invoice Finance, also known as factoring or accounts receivable financing, provides businesses with immediate access to working capital tied up in unpaid invoices. It’s a funding solution particularly beneficial for businesses experiencing growth, seasonal fluctuations, or those needing to improve cash flow management. Instead of waiting the standard 30, 60, or 90 days for customers to pay, IGF allows companies to leverage their invoices to unlock cash much sooner.

Here’s how it generally works: a business sells its unpaid invoices to IGF, a specialized financing company. IGF then advances a percentage of the invoice value, typically between 70% and 90%, to the business, providing them with immediate funds. Once the customer pays the invoice, IGF remits the remaining balance (minus their fees) to the business.

There are two main types of invoice finance: recourse and non-recourse. In recourse factoring, if the customer fails to pay the invoice due to insolvency or other reasons, the business is ultimately responsible for repurchasing the unpaid invoice from IGF. This option usually comes with lower fees. In non-recourse factoring, IGF assumes the risk of non-payment due to the customer’s creditworthiness. While this offers greater protection for the business, it generally involves higher fees and stricter due diligence on the customer.

IGF carefully assesses the creditworthiness of the business’s customers (the debtors) before providing financing. This evaluation helps them determine the risk associated with purchasing the invoices. The fees charged by IGF typically consist of a factoring fee, which is a percentage of the invoice value, and may also include other charges such as service fees and administrative costs.

Benefits of using IGF Invoice Finance:

- Improved Cash Flow: Immediate access to working capital allows businesses to meet their financial obligations, such as paying suppliers, salaries, and overhead costs.

- Growth Opportunities: Increased cash flow enables businesses to invest in expansion, new equipment, or marketing initiatives.

- Reduced Administrative Burden: Some IGF providers offer invoice management and collection services, freeing up internal resources.

- Flexibility: IGF is often a more flexible financing option compared to traditional bank loans, as it’s directly tied to sales revenue.

- Improved Credit Rating: By paying bills on time and maintaining healthy cash flow, businesses can improve their credit rating.

Considerations when choosing an IGF provider:

- Fees and Charges: Carefully compare the factoring fees, service fees, and other charges of different providers.

- Reputation and Experience: Choose a reputable IGF provider with a proven track record.

- Customer Service: Ensure the provider offers responsive and reliable customer service.

- Contract Terms: Understand the terms and conditions of the factoring agreement, including the recourse options and any termination clauses.

- Industry Expertise: Some IGF providers specialize in specific industries, which can be beneficial.

In conclusion, IGF Invoice Finance offers a valuable funding solution for businesses seeking to unlock working capital tied up in unpaid invoices. By carefully considering the different options and choosing the right provider, businesses can leverage IGF to improve their cash flow, fuel growth, and streamline their operations.

1024×588 igf invoice finance invoice factoring invoice discounting from invoice-funding.co.uk

1024×588 igf invoice finance invoice factoring invoice discounting from invoice-funding.co.uk  850×285 igf invoice finance companeouk from www.companeo.co.uk

850×285 igf invoice finance companeouk from www.companeo.co.uk  600×280 igf consulting igf logic from www.igf-logic.com

600×280 igf consulting igf logic from www.igf-logic.com  1530×1020 aldermore invoice finance invoice template ideas from simpleinvoice17.net

1530×1020 aldermore invoice finance invoice template ideas from simpleinvoice17.net  500×339 invoice finance sedge funding from sedgefunding.com

500×339 invoice finance sedge funding from sedgefunding.com  638×826 invoice finance expert infographics from www.slideshare.net

638×826 invoice finance expert infographics from www.slideshare.net  742×255 igf appoints invoice finance md igf independent growth finance from www.igfgroup.com

742×255 igf appoints invoice finance md igf independent growth finance from www.igfgroup.com  750×484 invoice finance prime finance from primefinance.co.nz

750×484 invoice finance prime finance from primefinance.co.nz  1080×608 invoice finance boost business cash flow octet from www.octet.com

1080×608 invoice finance boost business cash flow octet from www.octet.com  884×409 invoice report ifs community from community.ifs.com

884×409 invoice report ifs community from community.ifs.com  512×512 invoice finance comprehensive guide enlightened mindset from www.tffn.net

512×512 invoice finance comprehensive guide enlightened mindset from www.tffn.net  1024×750 invoice factoring invoice discounting infographic from tradefinanceglobal.com

1024×750 invoice factoring invoice discounting infographic from tradefinanceglobal.com  932×550 igf stock fund price chart nasdaqigf tradingview from www.tradingview.com

932×550 igf stock fund price chart nasdaqigf tradingview from www.tradingview.com  853×1024 invoice finance impulse capital from www.impulsecapital.co.uk

853×1024 invoice finance impulse capital from www.impulsecapital.co.uk  1024×731 invoiceinterchanges invoice finance facility helps businesses grow from www.invoiceinterchange.com

1024×731 invoiceinterchanges invoice finance facility helps businesses grow from www.invoiceinterchange.com  1520×500 invoice finance uk loan rates invoice financing loan from rosewoodfinance.co.uk

1520×500 invoice finance uk loan rates invoice financing loan from rosewoodfinance.co.uk  800×600 invoice finance facility unlock cash flow from growwithsupplychain.com

800×600 invoice finance facility unlock cash flow from growwithsupplychain.com  791×1024 roofing invoice sample invoice template ideas from simpleinvoice17.net

791×1024 roofing invoice sample invoice template ideas from simpleinvoice17.net  640×480 invoice finance benefits businesses mikegingerichcom from www.mikegingerich.com

640×480 invoice finance benefits businesses mikegingerichcom from www.mikegingerich.com  769×4746 invoice finance work business expert from www.businessexpert.co.uk

769×4746 invoice finance work business expert from www.businessexpert.co.uk  1152×648 invoice finance wilson field licensed insolvency practitioners from www.wilsonfield.co.uk

1152×648 invoice finance wilson field licensed insolvency practitioners from www.wilsonfield.co.uk  1417×1002 invoice finance office support fair pay services from www.fairpayservices.co.uk

1417×1002 invoice finance office support fair pay services from www.fairpayservices.co.uk  1200×1013 invoicefair twitter growth funding from twitter.com

1200×1013 invoicefair twitter growth funding from twitter.com  802×484 global igf update igf meeting virtual igf usa from www.igfusa.us

802×484 global igf update igf meeting virtual igf usa from www.igfusa.us  600×400 understanding invoice financing invoice factoring from rosewoodfinance.co.uk

600×400 understanding invoice financing invoice factoring from rosewoodfinance.co.uk  720×1018 guide invoice finance pulse cashflow finance factoring from www.slideserve.com

720×1018 guide invoice finance pulse cashflow finance factoring from www.slideserve.com  1024×750 invoice finance infographic trade finance finance infographic finance from www.pinterest.co.uk

1024×750 invoice finance infographic trade finance finance infographic finance from www.pinterest.co.uk