“`html

The break-even point is a critical concept in finance and business management. It represents the point at which total revenue equals total costs, meaning the business is neither making a profit nor incurring a loss. Understanding the break-even point is essential for pricing decisions, cost control, and overall financial planning.

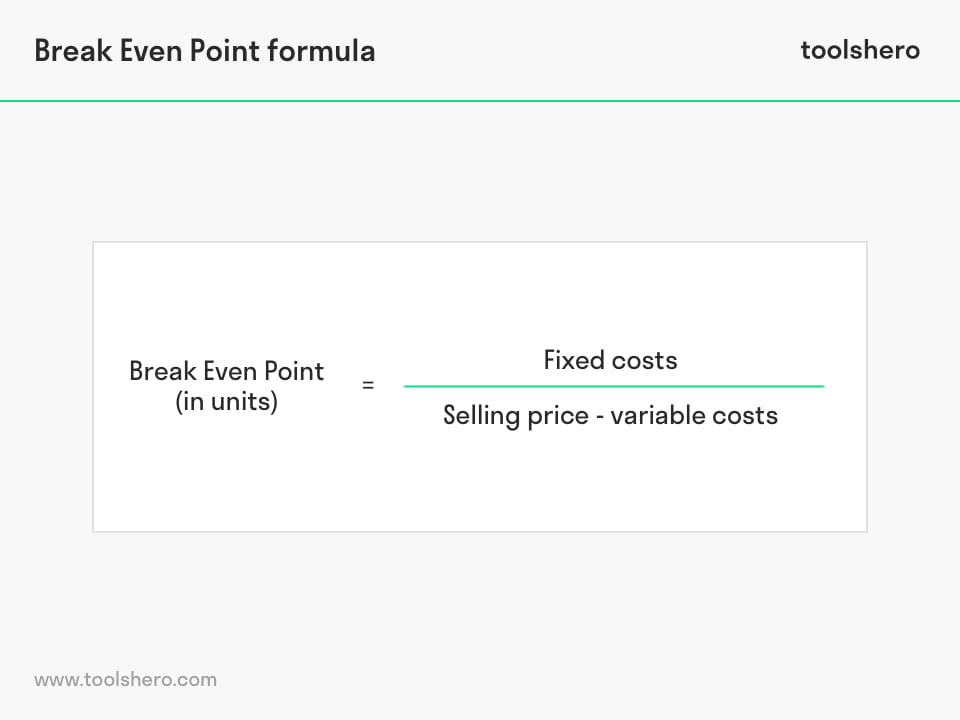

The break-even equation is the mathematical formula used to calculate this crucial threshold. There are two primary ways to express it: in units (the number of products or services that need to be sold) and in sales dollars (the total revenue needed to cover all costs).

Break-Even Point in Units:

The formula for calculating the break-even point in units is:

Break-Even Point (Units) = Fixed Costs / (Sales Price Per Unit – Variable Cost Per Unit)

Let’s break down each component:

- Fixed Costs: These are costs that remain constant regardless of the production volume or sales level. Examples include rent, salaries, insurance, and depreciation.

- Sales Price Per Unit: This is the revenue generated from selling one unit of the product or service.

- Variable Cost Per Unit: These are costs that vary directly with the level of production or sales. Examples include raw materials, direct labor, and sales commissions.

- (Sales Price Per Unit – Variable Cost Per Unit): This difference is also known as the contribution margin per unit. It represents the amount of revenue from each unit sold that contributes towards covering fixed costs and generating profit.

Break-Even Point in Sales Dollars:

The formula for calculating the break-even point in sales dollars is:

Break-Even Point (Sales Dollars) = Fixed Costs / Contribution Margin Ratio

Here’s a further explanation:

- Fixed Costs: As defined above, these are the constant expenses.

- Contribution Margin Ratio: This is the percentage of revenue that contributes to covering fixed costs and generating profit. It’s calculated as: (Sales Price Per Unit – Variable Cost Per Unit) / Sales Price Per Unit. It can also be calculated as: Total Sales – Total Variable Costs/Total Sales.

Using the Break-Even Equation:

Once the break-even point is calculated, it can be used for various purposes. For example, businesses can use it to determine the minimum sales volume required to avoid losses. It also allows them to assess the impact of changes in costs or pricing strategies on profitability. If a company anticipates a rise in fixed costs, the break-even analysis can show how many more units need to be sold, or how much prices need to be raised, to compensate. Additionally, the break-even analysis aids in setting realistic sales targets and making informed decisions about entering new markets or launching new products. By providing a clear understanding of the relationship between costs, sales, and profits, the break-even equation is a valuable tool for financial planning and decision-making.

“`

700×599 break equation finance tessshebaylo from www.tessshebaylo.com

700×599 break equation finance tessshebaylo from www.tessshebaylo.com  814×755 break equation dollars tessshebaylo from www.tessshebaylo.com

814×755 break equation dollars tessshebaylo from www.tessshebaylo.com  745×1053 break point equation tessshebaylo from www.tessshebaylo.com

745×1053 break point equation tessshebaylo from www.tessshebaylo.com  728×546 break equation units tessshebaylo from www.tessshebaylo.com

728×546 break equation units tessshebaylo from www.tessshebaylo.com  807×454 break point units mathematical equation tessshebaylo from www.tessshebaylo.com

807×454 break point units mathematical equation tessshebaylo from www.tessshebaylo.com  646×440 break analysis calculate break point from corporatefinanceinstitute.com

646×440 break analysis calculate break point from corporatefinanceinstitute.com  1384×476 break analysis equation from www.economicsonline.co.uk

1384×476 break analysis equation from www.economicsonline.co.uk  900×531 break formula determine profitability business udemy blog from blog.udemy.com

900×531 break formula determine profitability business udemy blog from blog.udemy.com .jpg) 1500×1108 calculate break point business paychex from www.paychex.com

1500×1108 calculate break point business paychex from www.paychex.com :max_bytes(150000):strip_icc()/break-even-analysis2-11ab7200a3924ae9bddb1bc6f4e5fd1f.png) 1500×1000 break analysis explained bilarasa from bilarasa.com

1500×1000 break analysis explained bilarasa from bilarasa.com  1200×1140 break formula templates google sheets microsoft excel from slidesdocs.com

1200×1140 break formula templates google sheets microsoft excel from slidesdocs.com  1200×675 break point analysis formula plan projections from www.planprojections.com

1200×675 break point analysis formula plan projections from www.planprojections.com  1754×1240 performance magazine marketing meets finance break level from www.performancemagazine.org

1754×1240 performance magazine marketing meets finance break level from www.performancemagazine.org  3200×2400 break analysis steps pictures wikihow from www.wikihow.com

3200×2400 break analysis steps pictures wikihow from www.wikihow.com  1200×1553 break analysis equation technique financial management studocu from www.studocu.com

1200×1553 break analysis equation technique financial management studocu from www.studocu.com  8001×4501 break analysis formula examples erp from 10xerp.com

8001×4501 break analysis formula examples erp from 10xerp.com  1200×600 break point formula bep calculate analyze from www.erp-information.com

1200×600 break point formula bep calculate analyze from www.erp-information.com  800×1192 break formula excel from mavink.com

800×1192 break formula excel from mavink.com  1024×768 break analysis powerpoint id from www.slideserve.com

1024×768 break analysis powerpoint id from www.slideserve.com  960×720 break analysis formula toolshero from www.toolshero.com

960×720 break analysis formula toolshero from www.toolshero.com  1589×1133 break analysis apparel industry ordnur from ordnur.com

1589×1133 break analysis apparel industry ordnur from ordnur.com