“`html

Finance Interpolation Formula: Bridging the Data Gaps

In finance, we often encounter situations where data is available for specific points in time, but we need to estimate values for intermediate dates. This is where interpolation comes in handy. Interpolation is a mathematical technique used to estimate values between known data points. It provides a reasonable approximation when exact data isn’t accessible.

Why Use Interpolation in Finance?

Interpolation is crucial in various financial applications:

- Yield Curve Construction: Treasury yields are typically quoted for standard maturities (e.g., 1 year, 5 years, 10 years). To determine the yield for a non-standard maturity (e.g., 7 years), interpolation is necessary.

- Pricing Derivatives: Many derivative pricing models require continuous forward rates. Interpolation helps create a continuous term structure from discrete market rates.

- Missing Data: Sometimes, data points are missing due to market closures or reporting errors. Interpolation fills these gaps, enabling more complete analysis.

- Smoothing Data: Interpolation can smooth out noisy data, providing a clearer picture of underlying trends.

Common Interpolation Methods

Several interpolation methods exist, each with its own assumptions and complexities. Here are some of the most frequently used in finance:

Linear Interpolation

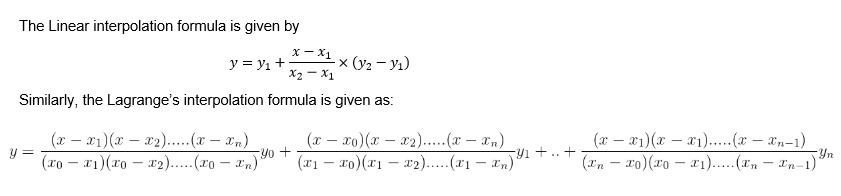

This is the simplest method. It assumes a linear relationship between the known data points. The formula is:

y = y1 + (x – x1) * (y2 – y1) / (x2 – x1)

Where:

- x is the point for which we want to estimate the value.

- x1 and x2 are the known data points surrounding x.

- y1 and y2 are the corresponding values at x1 and x2.

- y is the interpolated value.

Linear interpolation is easy to implement but may not be accurate if the relationship between the data points is non-linear.

Cubic Spline Interpolation

Cubic spline interpolation uses piecewise cubic polynomials to create a smooth curve that passes through the known data points. It offers a more accurate representation than linear interpolation, especially when dealing with non-linear relationships.

While the underlying math is more complex, many software packages (e.g., Python’s SciPy library, Excel) provide built-in functions for cubic spline interpolation.

Other Interpolation Methods

Besides linear and cubic spline interpolation, other techniques include:

- Exponential Interpolation: Useful for growth rates or values that increase exponentially.

- Log-Linear Interpolation: A variation suitable for yield curve construction, often preferred over linear interpolation.

- Nearest Neighbor Interpolation: Assigns the value of the closest known data point to the unknown point. Less accurate but useful in specific scenarios.

Choosing the Right Method

The choice of interpolation method depends on the specific application and the characteristics of the data. Consider the following factors:

- Accuracy: How precise does the estimate need to be?

- Smoothness: Does the interpolated curve need to be smooth?

- Computational Complexity: How easy is the method to implement?

- Data Characteristics: Is the relationship between the data points linear or non-linear?

In conclusion, interpolation is a vital tool in finance for estimating values between known data points. Understanding the different methods and their limitations allows for informed decisions and more accurate financial analysis.

“`

554×368 interpolation formula excel template from www.educba.com

554×368 interpolation formula excel template from www.educba.com  2325×1707 linear interpolation formula learn formula find linear from www.cuemath.com

2325×1707 linear interpolation formula learn formula find linear from www.cuemath.com  1200×628 interpolation formula linear lagrange interpolation examples from testbook.com

1200×628 interpolation formula linear lagrange interpolation examples from testbook.com  978×624 linear interpolation formula quick guide education from theeducationlife.com

978×624 linear interpolation formula quick guide education from theeducationlife.com  715×405 interpolation formula interpolate video lesson transcript from study.com

715×405 interpolation formula interpolate video lesson transcript from study.com  841×196 interpolation definition formula methods from byjus.com

841×196 interpolation definition formula methods from byjus.com  524×390 linear interpolation formulas from excelatfinance.com

524×390 linear interpolation formulas from excelatfinance.com  256×134 learning easy interpolation formula financial management from lmeasy.blogspot.com

256×134 learning easy interpolation formula financial management from lmeasy.blogspot.com  1280×720 interpolation formula excel template vrogueco from www.vrogue.co

1280×720 interpolation formula excel template vrogueco from www.vrogue.co  1200×630 linear interpolation definition formula mathful from mathful.com

1200×630 linear interpolation definition formula mathful from mathful.com  791×1119 linear interpolation equation formula calculator dokumentips from dokumen.tips

791×1119 linear interpolation equation formula calculator dokumentips from dokumen.tips  768×346 interpolation definition formula calculation examples from www.wallstreetmojo.com

768×346 interpolation definition formula calculation examples from www.wallstreetmojo.com  850×1202 proposed formula interpolation comparison from www.researchgate.net

850×1202 proposed formula interpolation comparison from www.researchgate.net  1000×690 linear interpolation calculator formula calculatorsio from calculators.io

1000×690 linear interpolation calculator formula calculatorsio from calculators.io  0 x 0 interpolation statistics definition formula video from study.com

0 x 0 interpolation statistics definition formula video from study.com  800×270 interpolation formula methods intellipaat from intellipaat.com

800×270 interpolation formula methods intellipaat from intellipaat.com  565×324 excel interpolation formulas peltier tech blog from peltiertech.com

565×324 excel interpolation formulas peltier tech blog from peltiertech.com  1024×768 image interpolation powerpoint id from www.slideserve.com

1024×768 image interpolation powerpoint id from www.slideserve.com  3200×2400 double linear interpolation pictures wikihow from www.wikihow.com

3200×2400 double linear interpolation pictures wikihow from www.wikihow.com  1286×922 interpolation methods support center from support.precisionlender.com

1286×922 interpolation methods support center from support.precisionlender.com  1200×1553 linear interpolation standard question finance from www.studocu.com

1200×1553 linear interpolation standard question finance from www.studocu.com  945×456 interpolation from docs.oracle.com

945×456 interpolation from docs.oracle.com